According to Section 41 of the Revenue Code of the Thai Revenue Department, foreigners have the duty to file their taxes in Thailand as below:

Income derived in Thailand

If a foreigner has income from sources within Thailand either by employment, own business or assets located in Thailand, such income is subject to income tax whether such income is paid within or outside Thailand.

Income derived outside Thailand

If a foreigner has income outside Thailand, such income is subject to Thailand income tax if these two conditions are met:

Such income has been incurred in any tax year starting from 1 January 2024 onward by a foreigner who stays in Thailand for 180 days or more in a tax year, and;

Such income earned from 1 January 2024 has been remitted or brought into Thailand (whether wholly or partially) in any tax year from 2024 onward

For instance, a Burmese who lives in Thailand for at least 180 days in 2024 with income from Myanmar or another country brings the money earned before 2024 into Thailand in 2024, then it will not be taxed. If he/she brings the money earned in 2024 into Thailand in 2025, then it will be taxed in 2025. However, if he/she has income earned outside Thailand but he/she is not a tax resident in Thailand and brought or remitted such income into Thailand later, it is not subject to Thai tax because he/she did not stay in Thailand for 180 days or more during the tax year.

Tax Returns to be Filed

If he has income derived from employment in Thailand only, he must submit the personal income tax return P.N.D. 91.

If he has income derived within Thailand and outside Thailand or just from outside Thailand, he must submit the personal income tax return P.N.D. 90.

MSNA Group can not only help Burmese people on how to do business in Thailand, we can also help you with Thailand taxes. If you need assistance in filing your personal income tax returns in Thailand, you come to the right place. Contact us now for more information.

Today, a client whom we helped register a 100% Myanmar owned export company in Thailand asked us if it is necessary for them to be registered in the VAT system. Here is our response:

Normally, a company is required to register into the VAT system if the gross sale has reached 1.8 million Baht in a year or the company hires foreigners and needs to apply for a work permit because the VAT registration certificate is one of the documents requested by the Thai immigration bureau. Anyway, the company may choose to register into the VAT system before that. And once you are registered into the VAT system, you have to submit your monthly VAT returns (PP.30) with or without sale transactions. You can decide to apply for VAT refund from the Revenue Department later but keep in mind that the tax officer will request to see all supporting documents before giving you the refund.

Thai Lawyers can help you register the company into the VAT system. MSNA Group can handle bookkeeping, accounting, tax filing and consultation on Thai taxes. We will ensure that you’re your documents are properly kept in files for easier reference when tax authorities request to see them. We can also assist you in representing your company with the Revenue Department especially when you apply for VAT refund. However, we will not be responsible to speed up the process because it is up to the tax officials when they can finish checking your documents and consider your application to claim VAT. You may find helpful information on what to do once a company is registered in the VAT system, and how withholding taxes in Thailand work.

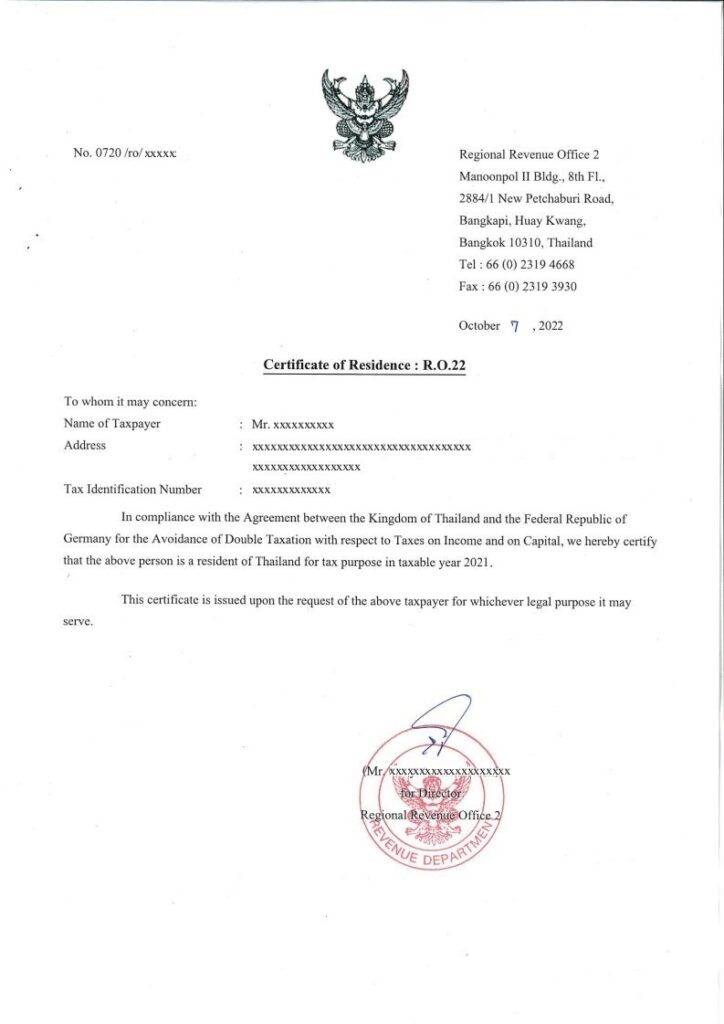

Who wants a Tax Residence Certificate or “Certificate of Residence”? Simply put, the foreigners who want to show it to their home country to prove that they should pay tax to Thailand and not their home country. Tax residence certificate may be issued by the Thai Revenue Department upon request by a foreigner who stayed in the country for 180 days or more in a calendar year. If you were in Thailand for such a period in many years, you need a Tax residence certificate for each year. Not one certificate is good for various years. By the way, do not confuse it with a Tax Clearance Certificate or an Income Tax Payment Certificate.

A company registered in Thailand may also request a tax residence certificate. However, here we want to talk only about individuals who may want to obtain one. MSNA Group can assist you in getting it issued by the Thai tax authorities. The two most important things are:

You need to be able to prove that you were in Thailand (continuously or not) at least 180 days in the year by showing the copy of your passport pages where there are stamps of your entries and exits.

You need to have income earned in that year and brought into Thailand the same year, or you were working in Thailand with a work permit. This way, you would file your personal income tax of that year. The Revenue Department needs to see your tax return with its official receipt and your Tax ID card.

Just contact MSNA Group so we can help you obtain your Tax ID card, prepare and file your tax return, get an Income Tax Payment Certificate or a Tax Clearance Certificate or a Tax Residence Certificate (which the Revenue Department calls “Certificate of Residence”). Essentially, the document looks like this:

What is an Income Tax Payment Certificate? When foreigners work in Thailand, they have to pay taxes here. Your Thai employer must get a work permit for you to be able to pay you legally. Every month when they pay you salary, they need to withhold your personal income tax and submit it to the Thai Revenue Department by the 7th of the following month (or 15th if they do it online). At the end of the year (or at the time you leave the company during the year), the employer must give you a document called 50 Tawi, or withholding tax certificate. The document has the detail of the total income you earned that year from this company, the total tax and the total social security amounts they withheld from you that year. However, it is not your Income Tax Payment Certificate.

When you prepare your personal income tax return at the beginning of the following year (31 March is the deadline), you will have to fill out the amount of tax withheld that is written in the withholding tax certificate. This tax is your tax credit. It is the tax you paid during the year by the employer’s withholding it from your income. If you did not have other sources of income from anywhere else, most likely you will not have to pay more taxes if your employer’s payroll team calculated your monthly withholding tax correctly. In some cases you will get a tax refund.

When you file your personal income tax return (PND90 or PND91 depending on whether you have income sources other than from work), you will get a receipt issued by the Revenue Department. This receipt is not enough of a proof to the Inland Revenue Service in your home country. You will need to request the Thai Revenue Department to issue an “Income Tax Payment Certificate”, which is in English and it is accepted as the proof that you paid taxes in Thailand.

An “Income Tax Payment Certificate” is not the same as a “Tax Resident Certificate”. The latter is the certificate issued by the Thai Revenue Department to certify that you were a tax resident in Thailand in the year it is issued for. Only when you have stayed in Thailand for 180 days or more in a calendar year can you request for a Tax Resident Certificate.

According to the Revenue Department, a taxpayer who resides in Thailand and receives dividends from a juristic company or partnership registered in Thailand is entitled to a tax credit of 3/7 of the amount of dividends received. In computing his assessable income, the taxpayer should gross up his dividends by the amount of the tax credit received. The amount of tax credit is creditable against his personal income tax liability of the same year.

Moreover, a taxpayer who resides in Thailand and receives dividends or shares of profits from a Thai registered company or a mutual fund whose tax has been withheld at source at the rate of 10% may choose to exclude such dividends from his assessable income when calculating his Personal Income Tax. However, in doing so, the taxpayer will be unable to claim any refund or credit as explained in the above paragraph.

Thai personal income tax returns must be filed within 31st March of the year following the year in which the income was received. Contact MSNA for computation and filing of your PIT returns before the due date and further consultation on Thai taxation.

Previously, our Thai Tax Expert talked about the changes made by the Revenue Department in the Thai tax laws, particularly in the Personal Income Tax rule for married couples. In this post, we want to give more information about the allowed deductible expenses, allowances and filing options for married couples.

Deductible Expenses

The expenses are divided equally among the spouses as the joint income proportion.

Allowances

Each spouse can use these allowances to calculate their income tax as follows:

Child allowance – each spouse can use Baht 15,000 (if the child is studying at the qualified level, each spouse can use Baht 17,000)

Home Loan Interest Deduction – each spouse is entitled up to Baht 100,000 of interest deduction. However, if they entered into a loan agreement together, each of them is entitled to Baht 50,000 of interest deduction.

Filing Options

A married couple may have 5 options in submitting their tax returns:

Each spouse files his/her tax returns separately;

They file their returns jointly, combining the wife’s income with the husband’s income and submit the tax returns under the husband’s name;

They file their returns jointly, combining the husband’s income with the wife’s income and submit the tax returns under the wife’s name;

They file their returns jointly but the husband files his Section 40(1) income separately;

They file their returns jointly but the wife files her Section 40(1) income separately.

Need help in filing your Thailand personal income tax returns? Contact MSNA now.

In one of our previous posts, we talked about Tax Clearance Certificate, which is a certificate issued by the Revenue Department to a non-Thai tax resident who is departing Thailand to indicate that he has already paid taxes or that he has provided a guarantor or securities as guarantee for tax liabilities and tax payable. In this post, we want to give more information about the types of tax clearance certificate in Thailand.

There are 2 types of Tax Clearance Certificate:

P. 3 Tax Clearance Certificate

This is issued to a foreigner who is temporarily departing Thailand. It is valid for a single departure and must be used within 15 days from the issuance date. If he/she could not depart Thailand within the specified period, P.3 Tax Clearance Certificate becomes invalid unless he/she renewed it before the expiry date.

P.3.1 Tax Clearance Certificate

This is issued to a foreigner who enters and leaves Thailand on a regular basis due to his/her business or profession. It is valid for multiple departure within the specified period in the Tax Clearance Certificate but not exceeding 180 days from the issuance date. P.3.1 Tax Clearance Certificate cannot be renewed.

Consult with MSNA how to get a Tax Clearance Certificate.

If you are a company operating in Thailand and pay overseas vendors for services, you will have to withhold some tax from the payments and submit it to the Thai Revenue Department within the 7th of the following month using form P.N.D. 54. The tax rates depend on the double taxation treaty between Thailand and vendors’ countries. If there is no such treaty, tax rate will be as stipulated in Thailand Revenue Code. Within the same period, paying to overseas suppliers, it also has to submit VAT return, form P.P. 36, which is the form that you submit 7% VAT on behalf of the vendor overseas. After you withhold the tax from the payment you make to the foreign vendors, sometimes you are requested by them to issue a withholding tax certificate for overseas vendors so that they can use the amount of tax withheld by you as a proof of their prepaid income tax.

How to get a withholding tax certificate for overseas vendors: You will have to get the withholding tax certificate in English from the Revenue Department and send it to them so they can use their tax credit in their country. The process will take 10-15 business day. You, as the payer, have to submit the following documents to Regional Revenue Office.

A copy of the filed withholding tax return i.e. P.N.D 54. and VAT return, P.P. 36

A copy of tax receipt issued by the Revenue Department

A copy of document indicating overseas remittance of payment and exchange rates.

A copy of service invoice

A copy of your company affidavit issued not over 1 month

Power of Attorney

Other relevant documents, such as copy of royalty agreement, passport or ID card copy of the authorized signatory and the agent’s.

Contact MSNA your Thailand accountant for tax and accounting needs.

Thailand inheritance tax and gift tax will start taking effect on 1 February, 2016. It is the first inheritance tax law in the country. 5% for ascendants or descendants and 10% for others are to be levied on inherited assets worth more than Baht 100 M. In order to prevent avoidance of the newly announced inheritance tax, Thailand gift tax is also introduced by amending the types of tax exempt income in the Thai Revenue Code. The gift tax will be enforced on the same day as the Inheritance Tax.

The inheritance tax is levied on heirs, both individuals and juristic persons. It is also applied to non-Thai nationals who are considered residents in Thailand according to Thailand immigration law and non-Thai inheriting assets which are located in Thailand.

The gift tax: Before 1 February 2016, the types of income exempt from personal income tax include income derived from maintenance, income derived from moral obligation, inheritance or a gift received in a ceremony or on other occasions in accordance with established custom. However, starting from 1 February 2016, only the following types of income are exempt from personal income tax:

1. The portion of inheritance income not more than Baht 100 M;

Income derived from the transfer of ownership or possessory right in an immovable property without consideration by the parent to a legitimate, non-adopted child, only for the portion not more than Baht 20 M per tax year;

Income derived from maintenance or gift from ascendants, descendants or spouse, only for the portion not more than Baht 20 M per tax year;

Income derived from maintenance under moral purposes or gift received in a ceremony or on occasions in accordance with custom and tradition from persons who are not ascendants, descendants or spouse, only for the portion not more than Baht 10 M per tax year; and

Income from gift received for use for religious, educational or public purposes according to the rules and conditions under a ministerial regulation yet to be issued.

For the taxpayers receiving income stated in No. 2 to 4 above, which exceeds the thresholds, may choose to pay tax at the rate of 5% and do not have to include those incomes in their annual personal income tax calculation/filing.

Consult with MSNA for your Thailand accounting and tax needs.

The businesses in Thailand welcomed a new law announced by the Thai government on 1 January 2016 that they may be eligible for being exempt from an audit by the Revenue Department on their income incurred within the accounting periods beginning before 1 January 2016. Here are the conditions:

Being a company or juristic partnership that did not have gross income exceeding THB 500 Million in the accounting period of 12 months ended within 31 December 2015;

Being a company or juristic partnership that is not being audited by the Revenue Department before 1 January 2016; and

Not being a company or juristic person that issues or uses fake VAT invoices or presents false expenses to the Revenue Department.

What do you have to do to enjoy this measure?

The company or juristic partnership must register for this measure on the website of the Thai Revenue Department between 15 January to 15 March 2016.

After the registration on the website, the company or juristic partnership must:

prepare its accounts and financial statements to reflect the real position of its business operation from the accounting period beginning on or after 1 January 2016;

file all tax returns applicable to its operation and submit taxes and duties completely from 1 January 2016 onward; and

not do anything to avoid paying taxes and duties.

If you do not fully comply with the above, the Revenue Depart will have the right to audit you.

Please note that even though your company has complied with all the above, if you seek a tax refund, the Revenue Department is empowered by the law to audit you for the purpose of processing the tax refund.

Consult with MSNA for your accounting and tax needs in Thailand.